intermediate accountingfifteenth edition ch11.docx

intermediate accountingfifteenth edition ch11.docx

- 文档编号:9632490

- 上传时间:2023-02-05

- 格式:DOCX

- 页数:113

- 大小:80.20KB

intermediate accountingfifteenth edition ch11.docx

《intermediate accountingfifteenth edition ch11.docx》由会员分享,可在线阅读,更多相关《intermediate accountingfifteenth edition ch11.docx(113页珍藏版)》请在冰豆网上搜索。

intermediateaccountingfifteentheditionch11

CHAPTER11

Depreciation,Impairments,andDepletion

ASSIGNMENTCLASSIFICATIONTABLE(BYTOPIC)

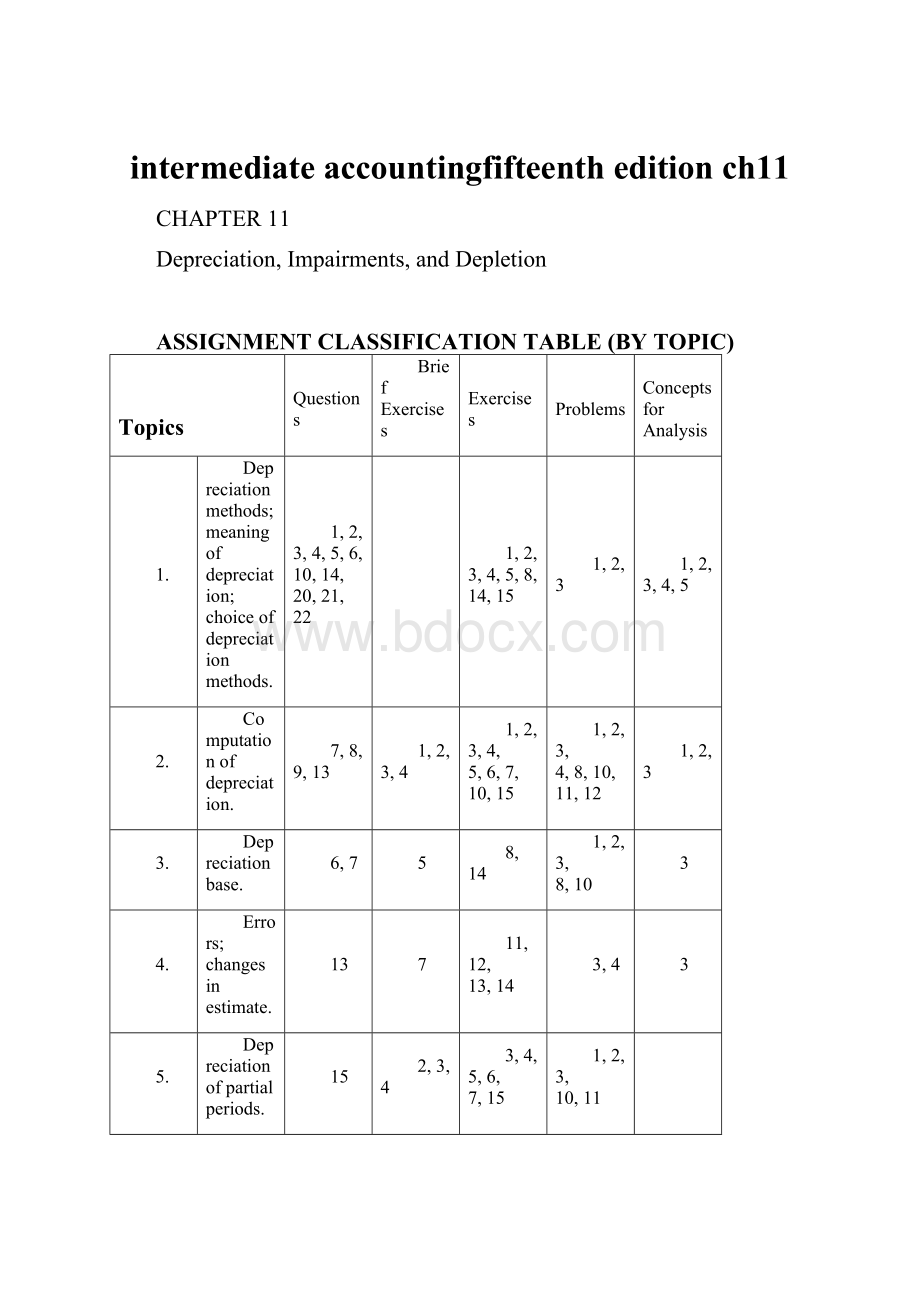

Topics

Questions

BriefExercises

Exercises

Problems

ConceptsforAnalysis

1.

Depreciationmethods;meaningofdepreciation;choiceofdepreciationmethods.

1,2,3,4,5,6,10,14,

20,21,22

1,2,3,4,5,8,14,15

1,2,3

1,2,3,4,5

2.

Computationof

depreciation.

7,8,9,13

1,2,3,4

1,2,3,4,

5,6,7,

10,15

1,2,3,

4,8,10,11,12

1,2,3

3.

Depreciationbase.

6,7

5

8,14

1,2,3,

8,10

3

4.

Errors;changesinestimate.

13

7

11,12,

13,14

3,4

3

5.

Depreciationofpartialperiods.

15

2,3,4

3,4,5,6,

7,15

1,2,3,

10,11

6.

Compositemethod.

11,12

6

9

2

7.

Impairmentofvalue.

16,17,

18,19

8

16,17,18

9

8.

Depletion.

22,23,24,25,26,27

9

19,20,21,22,23

5,6,7

9.

Ratioanalysis.

28

10

24

*10.

Taxdepreciation(MACRS).

29

11

25,26

12

*ThismaterialiscoveredinanAppendixtothechapter.

ASSIGNMENTCLASSIFICATIONTABLE(BYLEARNINGOBJECTIVE)

LearningObjectives

Questions

BriefExercises

Exercises

Problems

ConceptsforAnalysis

1.Explaintheconceptofdepreciation.

1

CA11-1

2.Identifythefactorsinvolvedinthedepreciationprocess.

2,3,4,5,6,7

1,2,3,4,5

1,2,3,4,5,6,

7,8,9,10,11,12,13,14,15

1,2,3,

4,8,10,11,12

CA11-2,CA11-3

3.Compareactivity,straight-lineanddecreasing-chargemethodsofdepreciation.

8,9,10

1,2,3,4,5

1,2,3,4,5,6,

7,8,10,11,12,13,14,15

1,2,3,4,5,8,10,11,12

CA11-4

4.Explainspecialdepreciationmethods.

11,12,13,14,15,16

6,7

9,11,12,13

CA11-5

5.Explaintheaccountingissuesrelatedtoassetimpairment.

17,18,19,20

8

16,17,18

9

6.Explaintheaccountingproceduresfordepletionofnaturalresources.

21,22,23,24,25,26,27

9

19,20,21,

22,23

5,6,7

7.Explainhowtoreportandanalyzeproperty,plant,equipment,andnaturalresources.

28

10

24

*8.Describeincometaxmethodsofdepreciation.

29

11

25,26

12

ASSIGNMENTCHARACTERISTICSTABLE

Item

Description

LevelofDifficulty

Time

(minutes)

E11-1

Depreciationcomputations—SL,SYD,DDB.

Simple

15–20

E11-2

Depreciation—conceptualunderstanding.

Moderate

20–25

E11-3

Depreciationcomputations—SYD,DDB—partialperiods.

Simple

15–20

E11-4

Depreciationcomputations—fivemethods.

Simple

15–25

E11-5

Depreciationcomputations—fourmethods.

Simple

20–25

E11-6

Depreciationcomputations—fivemethods,partialperiods.

Moderate

20–30

E11-7

Differentmethodsofdepreciation.

Simple

25–35

E11-8

Depreciationcomputation—replacement,nonmonetaryexchange.

Moderate

20–25

E11-9

Compositedepreciation.

Simple

15–20

E11-10

Depreciationcomputations,SYD.

Simple

10–15

E11-11

Depreciation—changeinestimate.

Simple

10–15

E11-12

Depreciationcomputation—addition,changeinestimate.

Simple

20–25

E11-13

Depreciation—replacement,changeinestimate.

Simple

15–20

E11-14

Erroranalysisanddepreciation,SLandSYD.

Moderate

20–25

E11-15

Depreciationforfractionalperiods.

Moderate

25–35

E11-16

Impairment.

Simple

10–15

E11-17

Impairment.

Simple

15–20

E11-18

Impairment.

Simple

15–20

E11-19

Depletioncomputations—timber.

Simple

15–20

E11-20

Depletioncomputations—oil.

Simple

10–15

E11-21

Depletioncomputations—timber.

Simple

15–20

E11-22

Depletioncomputations—mining.

Simple

15–20

E11-23

Depletioncomputations—minerals.

Simple

15–20

E11-24

Ratioanalysis.

Moderate

15–20

*E11-25

Bookvs.tax(MACRS)depreciation.

Moderate

20–25

*E11-26

Bookvs.tax(MACRS)depreciation.

Moderate

15–20

P11-1

Depreciationforpartialperiod—SL,SYD,andDDB.

Simple

25–30

P11-2

Depreciationforpartialperiods—SL,Act.,SYD,andDDB.

Simple

25–35

P11-3

Depreciation—SYD,Act.,SL,andDDB.

Moderate

40–50

P11-4

Depreciationanderroranalysis.

Complex

45–60

P11-5

Depletionanddepreciation—mining.

Moderate

25–30

P11-6

Depletion,timber,andextraordinaryloss.

Moderate

25–30

P11-7

Naturalresources—timber.

Moderate

25–35

P11-8

Comprehensivefixedassetproblem.

Moderate

25–35

P11-9

Impairment.

Moderate

15–25

P11-10

Comprehensivedepreciationcomputations.

Complex

45–60

ASSIGNMENTCHARACTERISTICSTABLE(Continued)

Item

Description

LevelofDifficulty

Time

(minutes)

P11-11

Depreciationforpartialperiods—SL,Act.,SYD,

andDDB.

Moderate

30–35

*P11-12

Depreciation—SL,DDB,SYD,Act.,andMACRS.

Moderate

25–35

CA11-1

Depreciationbasicconcepts.

Moderate

25–35

CA11-2

Unit,group,andcompositedepreciation.

Simple

20–25

CA11-3

Depreciation—strike,units-of-production,obsolescence.

Moderate

25–35

CA11-4

Depreciationconcepts.

Moderate

25–35

CA11-5

Depreciationchoice—ethics.

Moderate

20–25

SOLUTIONSTOCODIFICATIONEXERCISES

CE11-1

(a)Themasterglossaryprovidestwoentriesforamortization:

Amortization

Theprocessofreducingarecognizedliabilitysystematicallybyrecognizingrevenuesorreducingarecognizedassetsystematicallybyrecognizingexpensesorcosts.Inpensionaccounting,amortizationisalsousedtorefertothesystematicrecognitioninnetpensioncostoverseveralperiodsofamountspreviouslyrecognizedinothercomprehensiveincome,thatis,priorservicecostsorcredits,gainsorlosses,andthetransitionassetorobligationexistingatthedateofinitialapplicationofSubtopic715-30.

Amortization

Theprocessofreducingarecognizedliabilitysystematicallybyrecognizingrevenuesorbyreducingarecognizedassetsystematicallybyrecognizingexpensesorcosts.Inaccountingforpostretirementbenefits,amortizationalsomeansthesystematicrecognitioninnetperiodicpostretirementbenefitcostoverseveralperiodsofamountspreviouslyrecognizedinothercomprehensiveincome,thatis,gainsorlosses,priorservicecostorcredits,andanytransitionobligationorasset.

(b)Impairmentistheconditionthatexistswhenthecarryingamountofalong-livedasset(assetgroup)exceedsitsfairvalue.

(c)Recoverableamountisthecurrentworthofthenetamountofcashexpectedtoberecoverablefromtheuseorsaleofanasset.

(d)Accordingtotheglossary,thetermactivitiesistobeconstruedbroadly.Itencompassesphysicalconstructionoftheasset.Inaddition,itincludesallthestepsrequiredtopreparetheassetforitsintendeduse.Forexample,itincludesadministrativeandtechnicalactivitiesduringthepreconstructionstage,suchasthedevelopmentofplansortheprocessofobtainingpermitsfromgovernmentalauthorities.Italsoincludesactivitiesundertakenafterconstructionhasbeguninordertoovercomeunforeseenobstacles,suchastechnicalproblems,labordisputes,orlitigation.

CE11-2

AccordingtoFASBASC360-10-40-4through6(ImpairmentorDisposalofLong-LivedAssets...Long-LivedAssetstoBeExchangedortoBeDistributedtoOwnersinaSpinoff):

40-4ForpurposesofthisSubtopic,along-livedassettobedisposedofinanexchangemeasuredbasedontherecordedamountofthenonmonetaryassetrelinquishedortobedistributedtoownersinaspinoffisdisposedofwhenitisexchangedordistributed.Iftheasset(assetgroup)istestedforrecoverabilitywhileitisclassifiedasheldandused,theestimatedfuturecashflowsusedinthattestshallbebasedontheuseoftheassetforitsremainingusefullife,assumingthatthedisposaltransactionwillnotoccur.Insuchacase,anundiscountedcashflowsrecoverabilitytestshallapplypriortothedisposaldate.Inadditiontoanyimpairmentlossesrequiredtoberecognizedwhiletheassetisclassifiedasheldandused,andimpairmentloss,ifany,shallberecognizedwhentheassetisdisposedofifthecarryingamountoftheasset(disposalgroup)exceedsitsfairvalue.TheprovisionsofthisSectionapplytononmonetaryexchangesthatarenotrecordedatfairvalueundertheprovisionsofTopic845.

CE11-2(Continued)

40-5Againorlossnotpreviouslyrecognizedthatresultsfromthesaleofalong-livedasset(disposalgroup)shallberecognizedatthedateofsale.

40-6Seeparagraphs360-10-35-47through35-48forguidancerelatedtothedispositionofanassetuponitsabandonment.

CE11-3

AccordingtoFASBASC360-10-35-1through10(SubsequentMeasurement):

35-1ThisSubsectionaddressesproperty,plant,andequipment,subsequentmeasurementissuesrelatedtodepreciationandtheacquisitionofaninterestintheresidualvalueofaleasedasset.

35-2Thisguidanceaddressestheconceptofdepreciationaccountingandthevariousfactorstoconsiderinselectingtherelatedperiodsandmethodstobeusedinsuchaccounting.

35-3Depreciationexpenseinfinancialstatementsforanassetshallbedeterminedbasedontheasset’susefullife.

35-4Thecostofaproductivefacilityisoneofthecostsoftheservicesitrendersduringitsusefuleconomiclife.Generallyacceptedaccountingprinciples(GAAP)requirethatthiscostbespreadovertheexpectedusefullifeofthefacilityinsuchawayastoallocateitasequitablyaspossibletotheperiodsduringwhichservicesareobtainedfromtheuseofthefacility.Thisprocedureisknownasdepreciationaccounting,asystemofaccountingwhichaimstodistributethecostorotherbasicvalueoftangiblecapitalassets,lesssalvage(ifany),overtheestimatedusefullifeoftheunit(whichmaybea

- 配套讲稿:

如PPT文件的首页显示word图标,表示该PPT已包含配套word讲稿。双击word图标可打开word文档。

- 特殊限制:

部分文档作品中含有的国旗、国徽等图片,仅作为作品整体效果示例展示,禁止商用。设计者仅对作品中独创性部分享有著作权。

- 关 键 词:

- intermediate accountingfifteenth edition ch11

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

1212中级汽车维修工考试试题三.docx

1212中级汽车维修工考试试题三.docx

-

333教育综合.docx

-

204届毕业生基础知识考试试题 混凝土结构设计 试题.docx

-

100以内加减运算练习题.docx

-

101软件开发工程师JAVA初级考试样卷课件word版本.docx

-

CNN代码理解.docx

-

CPA审计第4章审计抽样下载版讲解.docx

-

hr培训管理系统.docx

-

318安通科科长岗位责任制.docx

-

2044施工现场环境污染的防治措施.docx

-

12371党务平台操作手册.docx

-

Catia百格线生成宏复习过程.docx

-

725kV及以上电压等级支柱瓷绝缘子运行规范.docx

-

1144甑底链板机说明书.docx

-

100个著名初等数学问题.docx

-

201X中学寒假工作计划范文.docx

-

111 生物的特征 练习 人教版七年级上册生物.docx

-

110KV变电所设计变压器翻译.docx

-

9920第二学期学校工作总结.docx

-

0911二级技能解答.docx

-

33415设计说明书正文.docx

-

311教育学基础综合大纲.docx

-

201浙江普通高校招生选考科目考试地理试题和答案解析.docx

-

C语言程序的设计实验实验指导书及答案.docx

-

272相似三角形的性质和判定.docx

-

ACCAHA不稳定型心绞痛和非ST段抬高心肌梗死治疗指南修订版摘要.docx

-

baosteel标准对照 外标含量.docx

-

M1模拟练习题.docx

-

ARM体系课程设计实验报告.docx

-

Android面试题整理.docx

-

gaoer.docx

-

CPⅢ测设方案.docx

-

部编版二年级语文上册复习计划复习精品Word格式文档下载.docx

-

创先争优简报20Word文档下载推荐.docx

-

G216一般路基土方技术交底Word下载.docx

-

70282考试指南及考题分享Word下载.docx

-

KPI绩效考核量化考核制度Word格式.docx

-

CloudStack 高级网络功能文档格式.docx

-

部编人教版三年级语文上册20美丽的小兴安岭课堂实录Word下载.docx

-

SPSS180试验指导版Word文档格式.docx

-

The report about the spare time of College studentsWord文件下载.docx

-

安徽省砀山二中学年高一下学期第一次月考政治试题 Word版含答案文档格式.docx

-

安全知识竞赛选拔赛精品试题库及答案共100题Word格式文档下载.docx

-

凹与凸的爱情世界Word格式.docx

-

巴中市中考英语押题卷与答案后附听力材料Word文件下载.docx

-

班级教师工作总结Word下载.docx

-

北大真题集Word文件下载.docx

-

北京工商大学教育学专业实习总结报告范文模板Word文件下载.docx

-

操作系统内存buddy算法和页置换算法实验报告Word下载.docx

-

部编版语文七年级下册第15课《驿路梨花》教案Word文档格式.docx

-

标准化检修手册静设备汇总整理Word格式.docx