亨格瑞管理会计英文第15版练习答案解析.docx

亨格瑞管理会计英文第15版练习答案解析.docx

- 文档编号:10981331

- 上传时间:2023-02-24

- 格式:DOCX

- 页数:93

- 大小:73.67KB

亨格瑞管理会计英文第15版练习答案解析.docx

《亨格瑞管理会计英文第15版练习答案解析.docx》由会员分享,可在线阅读,更多相关《亨格瑞管理会计英文第15版练习答案解析.docx(93页珍藏版)》请在冰豆网上搜索。

亨格瑞管理会计英文第15版练习答案解析

CHAPTER4

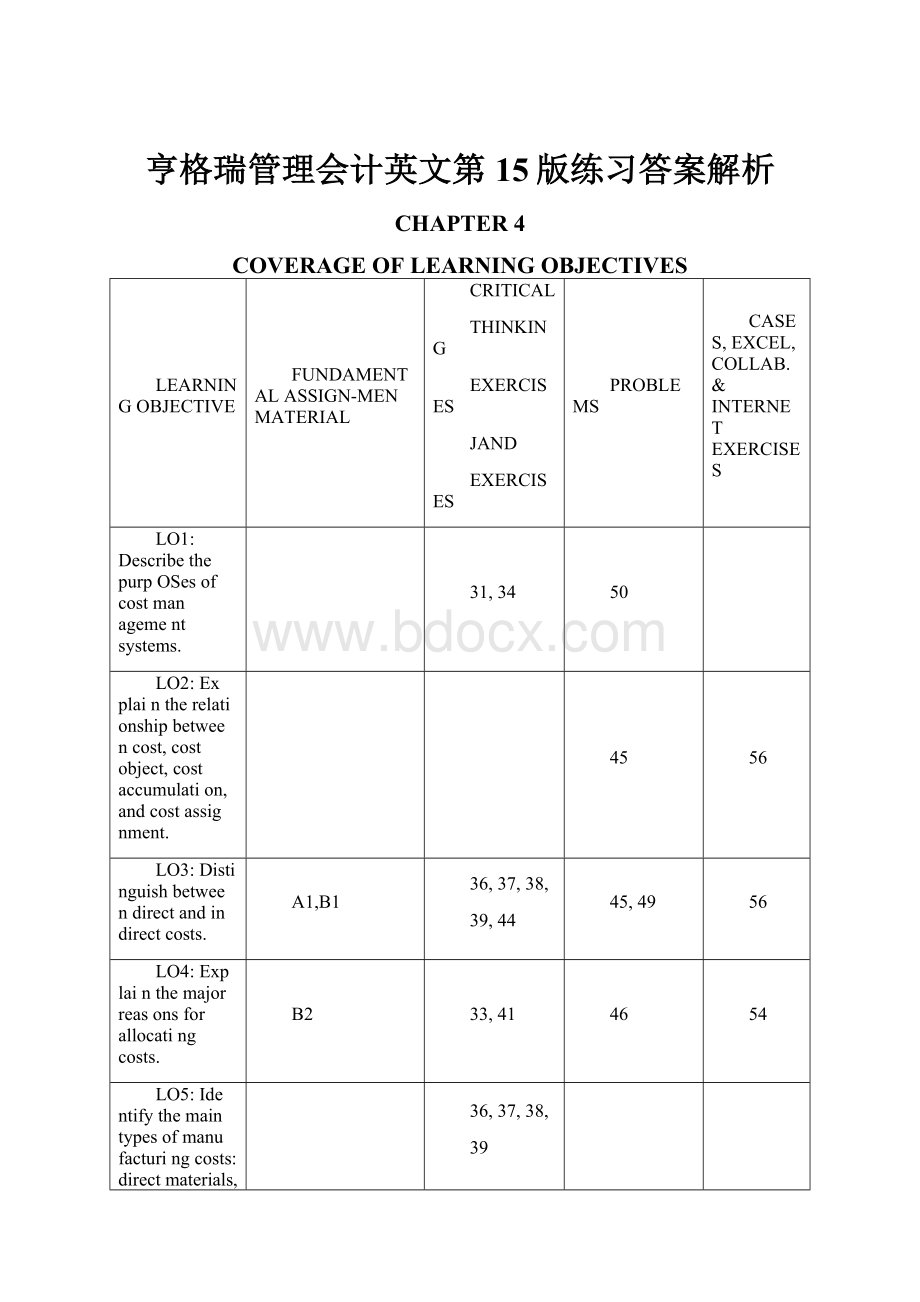

COVERAGEOFLEARNINGOBJECTIVES

LEARNINGOBJECTIVE

FUNDAMENTALASSIGN-MENMATERIAL

CRITICAL

THINKING

EXERCISES

JAND

EXERCISES

PROBLEMS

CASES,EXCEL,COLLAB.&INTERNETEXERCISES

LO1:

DescribethepurpOSesofcostmanagementsystems.

31,34

50

LO2:

Explaintherelationshipbetweencost,costobject,costaccumulation,andcostassignment.

45

56

LO3:

Distinguishbetweendirectandindirectcosts.

A1,B1

36,37,38,

39,44

45,49

56

LO4:

Explainthemajorreasonsforallocatingcosts.

B2

33,41

46

54

LO5:

Identifythemaintypesofmanufacturingcosts:

directmaterials,directlabor,andindirectproductioncosts.

36,37,38,

39

LO6:

Explainhowthefinancialstatementsofmerchandisersandmanufacturersdifferbecauseofthetypesofgoodstheysell.

A2

57,60,61

LO7:

Understandthemain

A3,A4,

33,40,41,

48,49,50

55,56,

differencesbetweentraditionalandactivitybasedcostingsystemsandwhyABCsystemsprovidevaluetomanagers.

B3,B4

42

57,58,

59,60,61

LO8:

Useactivity-basedcostinformationtomakestrategicandoperationalcontroldecisions.

A4,B4

32,37,43

48,49,50

55,56,60

CHAPTER4

CostManagementSystemsandActivity-BasedCosting

4-A1(20-30min.)

SeeTable4-A1onthefollowingpage.

4-A2

(25-30min.)

1.

MerchandiseInventories,1,000devices@$97

$97,000

2.

DirectmaterialsinventoryWork-in-processinventoryFinishedgoodsinventoryTotalinventories

$40,000

0

97,000

$137,000

3.

NILEELECTRONICSPRODUCTS

StatementofOperatingIncome

FortheYearEndedDecember31,20X9

Sales(9,000unitsat$170)

Costofgoodssold:

Beginninginventory

Purchases

Costofgoodsavailableforsale

Lessendinginventory

$0970,000

$970,000

97,000

$1,530,000

Costofgoodssold(anexpense)

Grossmarginorgrossprofit

Lessotherexpenses:

selling&administrativecosts

Operatingincome(alsoincomebeforetaxes

873,000

$657,000

185,000

$472,000

inthisexample)

Totalweightshippedis25,000kg+75,000kg+160,000kg=260,000kg.Indirectdistributioncostsper

kilogramisthen$10,400宁260,000kg=$0.04.Theallocationtocustomdetailedis$0.04x25,000kg=

$1,000.

STATEMENTOFOPERATINGINCOMEEXTERNALREPORTINGPURPOSE

OPERATINGINCOMEBYPRODUCTLINE

INTERNALSTRATEGICDECISIONMAKINGPURPOSE

Sales

$155,000

CustomLargeSmall

DetailedStd.Std.CostType,AssignmentMethod

$30,000$45,000$80,000

Costofgoodssold:

Directmaterial

40,000

5,00015,00020,000Direct,DirectTrace

Indirectmanufacturing

41,000

28,00015,0008,000Indirect,Alloc.-Mach.

Hours

81,000

33,00020,00028,000

Grossprofit

74,000

(3,000)25,00052,000

Sellingandadministrativeexpenses:

Commissions

15,000

1,5003,50010,000Direct,DirectTrace

Distributiontowarehouses

10,400

1,00023,0006,400Indirect,Allocation-Weight

Totalsellingandadmin.expenses

25,400

2,5006,50016,400

Contributiontocorporateexpensesandprofit

48,600

$(5,500)$18,500$35,600

Unallocatedexpenses:

Administrativesalaries

8,000

Otheradministrativeexpenses

4,000

Totalunallocatedexpenses

12,000

Operatingincomebeforetax

$36,600

1Totalmachinehoursis1,400+250+400

=2,050.Indirectmanufacturingcostpermachinehouristhen

TABLE4-A1

$41,000宁2,050=$20.Theallocationtocustomdetailedis$20x1,400machinehours=$28,000.

2

技术资料专业整理

4.

ORINOCO,INC.

StatementofOperatingIncome

FortheYearEndedDecember31,20X9

Sales(9,000unitsat$170)

$1,530,000

Costofgoodsmanufacturedandsold:

BeginningfinishedgoodsinventoryCostofgoodsmanufactured:

BeginningWIPinventoryDirectmaterialsusedDirectlaborIndirectmanufacturingTotalmfg.coststoaccountforLessendingwork-in-processinventory

CostofgoodsavailableforsaleLessendingfinishedgoodsinventoryCostofgoodssold(anexpense)Grossmarginorgrossprofit

Lessotherexpenses:

sellingandadministrativecostsOperatingincome(alsoincomebeforetaxesinthisexample)

290,000150,000

$970,000

530,000

970,000

$970,000

97,000

873,000

$657,000

185,000

$472,000

5.

Thebalaneesheetforthemerchandiser(Nile)hasjustonelineforinventories,theendinginventoryoftheitemspurchasedforresale.Thebalaneesheetforthemanufacturer(Orinoco)hasthreeitems:

directmaterialsinventory,work-in-processinventory,andfinishedgoodsinventory.

Theincomestatementsaresimilarexceptforthecomputationofcostofgoodsavailableforsale.Themerchandiser(Nile)simplyshowspurchasesfortheyearplusbeginninginventory.Incontrast,themanufacturer(Orinoco)showsbeginningwork-in-processinventoryplusthethreecategoriesofcostthatcomprisemanufacturingcost(directmaterialsused,directlabor,andfactory(ormanufacturing)overhead)andthendeductstheendingwork-in-processinventory.Themanufacturerthenaddsthebeginningfinishedgoodsinventorytothiscostofgoodsmanufacturedtogetthecostofgoodsavailableforsale.

6.Thepurposeisprovidingaggregatemeasuresofinventoryvalueandcost

ofgoodsmanufacturedforexternalreportingtoinvestors,creditors,andotherexternalstakeholders.

Banks

Therecanbemanyjustifiableanswersforeachitemotherthanthelistedcostdriverandbehavior.ThepurposeofthisexerciseistogenerateanactivediscussionregardingthosechosenbyFirstmanagers.Onepointthatshouldbeemphasizedisthatmanytimesmanagerschoosecostdriversthatarenotthemostplausibleorreliablebecauseoflackofdataavailability.Costdriversarealsousedasabasistoallocateactivityandresourcecostsandsotheavailabilityofdataisoftenanimportantconsideration.

a.*

b.**

c.

d.

e.

f.

c.***

h.

i.

j.

k.

l.

ActivityOrResourceRRRARRAARRRA

CostDriver

Numberofsquarefeet

Numberofpersonhours

Numberofcomputertransactions

Numberofschedules

Numberofpersonhours

Numberofloaninquiries

Numberofinvestments

Numberofapplications

Numberofpersonhours

Numberofminutes

Numberofpersonhours

Numberofloans

CostBehavior

F

F

V

*Anargumentcanbemadethatmaintenanceofthebuildingisanactivity.Ifthiswasthecase,resourcessuchassuppliesandlaborwouldberesourcesconsumed,andseveralresourcecostdriverswouldbeneeded.Inaddition,aseparateresourceandassociatedcostdriverwouldbeneededforinsuraneecosts.However,thecompanyhadacontractformaintenance(fixedprice),sothiswasafixed-costresourcethatwasaddedtootheroccupancycostssuchasinsuranee.Thecostdriverchosenforalltheseoccupancycostswassquarefeetoccupiedbythevariousdepartments.

backonlabor).Thisisanexampleofastepcostthatisfixedoverwiderangesofcost-driverlevel.

***Studentsmaytrytodeterminethecostbehaviorofactivitieseventhoughtheproblemrequirementsdonotaskforit.Pointoutthatactivitiesalmostalwayshavemixedcostbehaviorbecausetheyconsumevariousresources.Someofthesearefixed-costandothersvariable-costresources.Forexample,theactivity“researchtoevaluatealoanapplication”consumessuchfixed-cost

resourcesasmanagerlabortimeandcomputers(assumedownedbythebank).

Thisactivityalsoconsumesvariable-costresourcessuchastelecommunicationstimeandexternalcomputingservices.

(20-30min.)

4-A4

1.

Thefirststepistodeterminethecostpercost-driverunitforeachactivity:

Activity[Costdriver]

Monthly

Manufacturing

Overhead

Cost

Driver

Activity

CostperDriverUnit

MaterialHandling[Directmaterialscost]

$12,000

$200,000

$0.06

Engineering[Engineeringchangenotices]

20,000

20

1,000.00

Power[Kilowatthours]

16,000

400,000

0.04

TotalManufacturingOverhead

$48,000

Next,thecostsofeachactivitycanbeallocatedtoeachofthethreeproducts:

PHYSICALFLOW/ALLOCATEDCOST

CostSeniorBasicDeluxe

MaterialHandling$.06X25,000=$1,500$.06

Engineering$1,000X13=13,000$1,000X5=5,000$1,000

Power$.04X50,000=2,000$.04X200,000=8,000$.04

Total

X125,000=$7,5

2,000

2.

$16,500

Overheadratebasedondirectlaborcosts:

X50,000=$3,000$.06

X2=

X150,000=6,000

$15,500

$16,000

Rate=Totalmanufacturingoverhead

=$48,000-$8,000=$6.00/DL$

宁Totaldirectlaborcost

Overheadallocatedtoeachproductis:

Senior:

$6.00X4,000

Basic:

$6.00X1,000

$24,000

6,000

Deluxe:

Total

$6.00X3,000

18,000

$48,000

NoticethatmuchlessmanufacturingoverheadcostisallocatedtoBasicusingdirectlaborasacostdriver.Why?

BecauseBasicusesonlyasmallamountoflaborbutlargeamountsofotherresources,especiallypower.

“best.”

3.Theproductcostsinrequirement1aremoreaccurateifthecostdriversaregoodindicatorsofthecausesofthecosts--theyarebothplausibleandreliable.Forexample,kilowatthoursiscertainiyabettermeasureofthecostofpowercoststhanisdirectlaborhours.Therefore,theallocationofpowercostsinrequirement1iscertainIybetterthaninrequirement2.Materialshandlingandengineeringarelikewisemoreplausible.Amanagerwouldbemuchmoreconfidentinthemanufacturingoverheadallocatedtoproductsinrequirement1.Remember,however,thatthereareincrementalcostsofdatacollectionassociatedwiththemoreaccurateABCsystem.Thebenefit/costcriteriamustbeappliedindecidingwhi

- 配套讲稿:

如PPT文件的首页显示word图标,表示该PPT已包含配套word讲稿。双击word图标可打开word文档。

- 特殊限制:

部分文档作品中含有的国旗、国徽等图片,仅作为作品整体效果示例展示,禁止商用。设计者仅对作品中独创性部分享有著作权。

- 关 键 词:

- 亨格瑞 管理 会计 英文 15 练习 答案 解析

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

《城市规划基本知识》深刻复习要点.docx

《城市规划基本知识》深刻复习要点.docx

-

《高电压技术》word版.docx

-

《安全带》gb6095.docx

-

BCP计划应急计划.docx

-

《计算机组成与工作原理》第一章复习题.docx

-

CANON LBP系列激光打印机使用方法指南.docx

-

C语言课程设计火车票系统源代码.docx

-

3热力管道沟槽开挖方法.docx

-

HR岗位职责.docx

-

1 脱硫脱硝cems维护技术规范.docx

-

O2O超市商业项目计划书.docx

-

SCI期刊呼吸胸外.docx

-

18岁生日祝福语短信.docx

-

ITMC物流企业经营沙盘比赛规则.docx

-

XX钢绳成本管理.docx

-

Matlab的第三方工具箱大全强烈推荐.docx

-

安全保卫工作先进个人.docx

-

安全生产工作日记.docx

-

windows 漏洞集合.docx

-

Φ160数控落地镗铣床技术规格.docx

-

安全施工组织设计.docx

-

安全检查和隐患排查治理制度及记录.docx

-

部编版小学二年级语文下册课外阅读专项.docx

-

变电站投运前质量监督检查汇报材料模版.docx

-

版 创新设计 高考总复习 历史 北师大版第一部分 必考内容第十五单元 第38讲.docx

-

本科毕业设计论文.docx

-

北京大学社会心理学串讲笔记1一10章加试题.docx

-

亳州市教坛新星骨干教师学科带头人特级教师年度考核细则知识分享.docx

-

超星尔雅《人生与人心》期末考试满分答案.docx

-

财经法规与会计职业道德案例分析题.docx

-

茶文化会发言稿.docx

-

财务会计核算实习总结.docx

-

最新版机械设计制造及其自动化专业设计普通车床的数控化改造研究毕业论文设计.docx

-

学校公共卫生突发事件报告卡.docx

-

养生指导.docx

-

最新部编版四年级语文上册 第1单元 课时练.docx

-

学校饮用水工作总结.docx

-

冶金企业炼铁安全生产标准化评定标准.docx

-

最新地理高二四川省雅安市高二上学期期末考试word版.docx

-

雅思考试口语考题回顾Mar 810 17.docx

-

一幅漫画的启示作文范文37篇.docx

-

最新个人年终工作总结通用版.docx

-

兖矿集团榆林项目未批先建 百亿投资毁林上千亩.docx

-

小学校长个人工作总结最新.docx

-

最新届高考语文质量检测试题36新题型教师版+学生版直接可打印全国通用解析版.docx

-

一年级安全教育教学案.docx

-

养老服务业地方财政研究.docx

-

最新年党课思想汇报三篇.docx

-

一年级下册教案50.docx

-

小学一年级数学下册口算天天练84986.docx

-

医保定点零售药店日常管理制度.docx