中级会计学 intermediate accounting 赖红宁 chapter 4课后答案.docx

中级会计学 intermediate accounting 赖红宁 chapter 4课后答案.docx

- 文档编号:8687021

- 上传时间:2023-02-01

- 格式:DOCX

- 页数:88

- 大小:60.89KB

中级会计学 intermediate accounting 赖红宁 chapter 4课后答案.docx

《中级会计学 intermediate accounting 赖红宁 chapter 4课后答案.docx》由会员分享,可在线阅读,更多相关《中级会计学 intermediate accounting 赖红宁 chapter 4课后答案.docx(88页珍藏版)》请在冰豆网上搜索。

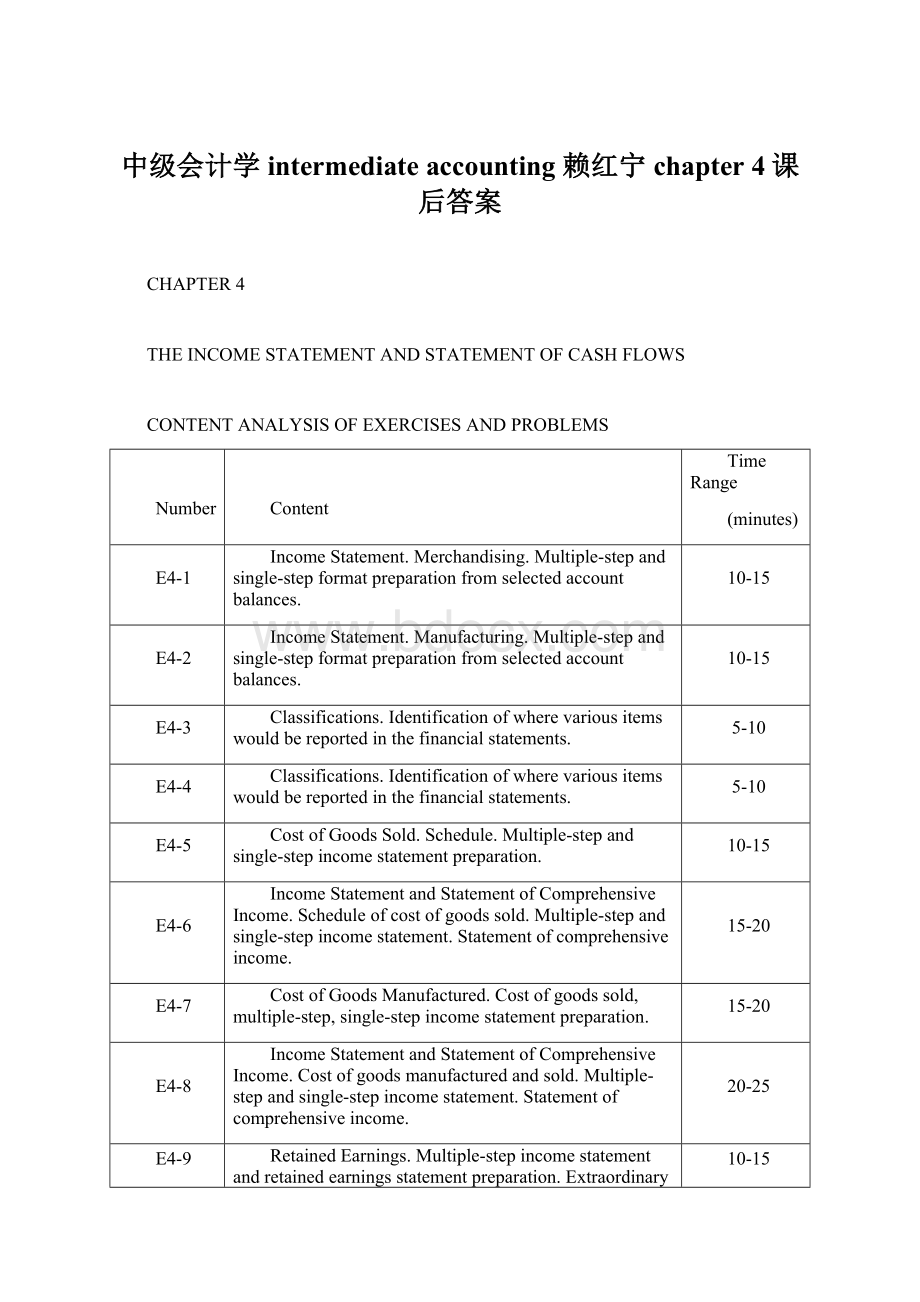

中级会计学intermediateaccounting赖红宁chapter4课后答案

CHAPTER4

THEINCOMESTATEMENTANDSTATEMENTOFCASHFLOWS

CONTENTANALYSISOFEXERCISESANDPROBLEMS

Number

Content

TimeRange

(minutes)

E4-1

IncomeStatement.Merchandising.Multiple-stepandsingle-stepformatpreparationfromselectedaccountbalances.

10-15

E4-2

IncomeStatement.Manufacturing.Multiple-stepandsingle-stepformatpreparationfromselectedaccountbalances.

10-15

E4-3

Classifications.Identificationofwherevariousitemswouldbereportedinthefinancialstatements.

5-10

E4-4

Classifications.Identificationofwherevariousitemswouldbereportedinthefinancialstatements.

5-10

E4-5

CostofGoodsSold.Schedule.Multiple-stepandsingle-stepincomestatementpreparation.

10-15

E4-6

IncomeStatementandStatementofComprehensiveIncome.Scheduleofcostofgoodssold.Multiple-stepandsingle-stepincomestatement.Statementofcomprehensiveincome.

15-20

E4-7

CostofGoodsManufactured.Costofgoodssold,multiple-step,single-stepincomestatementpreparation.

15-20

E4-8

IncomeStatementandStatementofComprehensiveIncome.Costofgoodsmanufacturedandsold.Multiple-stepandsingle-stepincomestatement.Statementofcomprehensiveincome.

20-25

E4-9

RetainedEarnings.Multiple-stepincomestatementandretainedearningsstatementpreparation.Extraordinaryitem,dividends,operatingloss.Computereturnonstockholders'equity.

10-15

E4-10

RetainedEarnings.Costofgoodssold,single-stepincomestatement,retainedearningsstatementpreparation.Extraordinaryitem,operatingloss,obsoletematerials,dividends.Computeprofitmargin.

15-20

E4-11

IncomeStatementCalculations.Determinationofvariousamountsforamerchandisingconcern.

10-15

Number

Content

TimeRange

(minutes)

E4-12

IncomeStatementCalculations.Determinationofvariousamountsforamanufacturer.

15-20

E4-13

ResultsofDiscontinuedOperations.Preparationofresultsfromdiscontinuedoperationssectionwhencomponentisheldforsaleatendofyear.

10-15

E4-14

ResultsofDiscontinuedOperations.Preparationofresultsfromdiscontinuedoperationssectionwhencomponentisheldforsaleatendofyear.

15-20

E4-15

(AICPAadapted).IncomeStatementDeficiencies.Identifyappropriateandinappropriatedisclosures.Providerationale.

20-25

E4-16

ComprehensiveIncome.Preparationofincomestatementandstatementofcomprehensiveincomeundertwodifferentmethods.

10-15

E4-17

NetCashFlowFromOperatingActivities.Preparationofoperatingactivitiessectionofstatementofcashflowsfromlistofitems.

5-15

E4-18

OperatingCashFlows:

DirectMethod.Preparecashflowsfromoperatingactivitiessectionofstatementofcashflows,usingthedirectmethod.

10-15

E4-19

StatementofCashFlows.Preparesimplestatementofcashflowsfromalistofitems.

10-15

E4-20

StatementofCashFlows.Preparesimplestatementofcashflowsfromalistofitems.

10-15

P4-1

ComprehensiveIncome.Formatpreparationofmultiple-stepincomestatement,statementofcomprehensiveincome,andretainedearningsstatement.

40-60

P4-2

Classifications.Matchingofvariousitemswithreportingcomponentinthefinancialstatements.

15-30

P4-3

IncomeStatement.Lowerportion.Dividends,componentdisposal,extraordinaryitem,priorperiodcorrection,changeinaccountingprinciple.Retainedearningsstatement.

20-40

P4-4

IncomeStatement.Lowerportion.Dividends,priorperiodcorrection,extraordinaryitem,changeinaccountingestimate,saleofdivision.Retainedearningsstatement.

20-40

P4-5

Comprehensive.Merchandisingincomestatement.Supportingschedules,single-stepincomestatement,retainedearningsstatement.Calculationofprofitmarginanddiscussion.

45-60

Number

Content

TimeRange

(minutes)

P4-6

Comprehensive.Merchandisingincomestatement.Supportingschedules,multiple-stepincomestatement,retainedearningsstatement.Computationofreturnonstockholders'equityanddiscussion.

40-60

P4-7

Comprehensive.Manufacturingincomestatement.Supportingschedules,multiple-stepincomestatement,retainedearningsstatement.Computationofreturnonstockholders'equityanddiscussion.

45-60

P4-8

Misclassifications.Identificationofincorrectlyclassifieditems.Preparationofacorrectmultiple-stepincomestatementandretainedearningsstatement.

30-45

P4-9

Misclassifications.Preparationofacorrectlyclassifiedmultiple-stepincomestatementandretainedearningsstatementfromonethatismisclassified.

20-40

P4-10

Classification.Recognitionofunusualand/orinfrequentitemsandindicationofwheretodisclose.

30-45

P4-11

ResultsofDiscontinuedOperations.Preparationofjournalentryforlossonheld-for-saledivision.Preparationofincomestatementincludingresultsfromdiscontinuedoperationssection.Preparationofpartialbalancesheet.

40-60

P4-12

IncomeStatementandCashFlowStatementDisclosures.QuestionsrelatingtothereviewofTheCoca-ColaCompanyincomestatementandcashflowstatementdisclosuresinAppendixA.

20-40

P4-13

(AICPAadapted).ComplexIncomeStatement.Preparationofmultiple-stepincomestatement,includingresultsofdiscontinuedoperationsandextraordinaryitem.

30-45

P4-14

(AICPAadapted).ComplexIncomeStatement.Preparationofmultiple-stepincomestatement,includingresultsofdiscontinuedoperationsandcumulativeeffect.

30-45

P4-15

(AICPAadapted).IncomeStatements.Comparative.Preparationofamultiple-stepcomparativestatementofincome.

30-45

P4-16

(AICPAadapted).FinancialStatementDeficiencies.Identificationofnon-arithmeticerrors.

30-45

P4-17

(AICPAadapted).ViolationsofGAAP.Identificationandsuggestedcorrectiveaction.

30-45

P4-18

Comprehensive:

ComparativeIncomeStatements.Preparationofcomparativeincomestatements.

20-30

Number

Content

TimeRange

(minutes)

P4-19

NetIncomeandComprehensiveIncome.Preparationofincomestatementandreportingofcomprehensiveincomeusingthreedifferentmethods.

20-30

P4-20

StatementofCashFlows.Preparationofthestatementofcashflowsfromalistofselecteditems.

10-20

P4-21

StatementofCashFlows.Preparationofthestatementofcashflowsfromalistofselecteditems.

10-20

P4-22

StatementofCashFlows:

DirectMethod.Preparationofthestatementofcashflows,usingthedirectmethodforoperatingactivities,fromalistofselecteditems.

10-20

P4-23

Comprehensive:

BalanceSheetandCashFlows.Preparationfromabeginningbalancesheetandanendingstatementofcashflows.

20-40

ANSWERSTOQUESTIONS

Q4-1Underthecapitalmaintenanceconcept,incomeforanaccountingperiodistheamountthatmaybepaidtostockholders(orowners)duringthataccountingperiodandstillenablethecorporationtobeaswelloffattheendoftheperiodasitwasatthebeginning.Thecapitalofacorporation(i.e.,itsassetsandliabilities)atthebeginningandendoftheperiodmaybemeasuredinavarietyofdifferentways.Thesealternativewaysofmeasuringthenetassetvalue(fromwhichincomeissubsequentlydetermined)underthecapitalmaintenanceconceptare:

(1)thepresentvalueoffuturecashflows,

(2)thenetrealizablevalue,(3)thecurrentmarketvalue,(4) thecurrentcost,or(5)thehistoricalcost.

Q4-2Inthetransactionalapproach,acompanyrecordsitsnetassetsattheirhistoricalcostanditdoesnotrecordchangesintheseassetsandliabilitiesunlessatransaction,event,orcircumstancehasoccurredthatprovidesreliableevidenceofachangeinvalue.Thetransactionalapproachisappliedusingtheaccrualbasisofaccounting.Inaccrualaccounting,acompanyrecordsthefinancialimpactsoftransactionsandothereventsandcircumstancesintheperiodsinwhichtheyoccurratherthanonlyintheperiodsinwhichitreceivesorpayscash.Thisistheapproachtoincomemeasurementthatcurrentlyisusedinaccounting.

Thetransactionalapproachisconsistentwiththecapitalmaintenanceconceptbasedonhistoricalcostsincetheincomerepresentsthedifferencebetweenthebeginningandendingadjustednetassetsonahistoricalcostbasis.However,theaccrual-basedtransactionalapproachtoincomemeasurementismoreinformativebecauseitrelates(matches)theaccomplishmentsandtheeffortssothatthereportedincomemeasurestheperformanceofacompany'searningsactivities.

Q4-3Comprehensiveincomeisthechangeinequityofacompanyduringaperiodfromtransactions,otherevents,andcircumstancesrelatedtononownersources.Itincludesallchangesinequityduringaperiodexceptthoseresultingfrominvestmentsbyownersanddistributionstoowners.

TheintentoftheFASBistwofold:

(1)todevelopaconceptofincomebroadenoughtoincludechangesinvaluenottraditionallyreportedinnetincomeunderthetransactionalapproach,and

(2) toallowforflexibilityastowherecertaincomponentsofincomearereportedinthefinancialstatements.

Q4-4(a)Returnoninvestmentisameasureofoverallcompanyperformance.Stockholders(investors)investcapitalinordertoobtainareturnoncapital.Beforeacompanycanprovideareturnoninvestment,itscapitalmustbemaintained.

(b)Riskistheuncertaintyorunpredictabilityofthefutureresultsofacompany.Thegreatertherangeandtimeframewithinwhichfutureresultsarelikelytofall,thegreatertheriskassociatedwithaninvestmentinorextensionofcredittothecompany.Generally,thegreatertherisk,thehighertherateofreturnexpected.

(c)Financialflexibilityistheabilityofacompanytoadapttounexpectedneedsandopportunities.Financialflexibilitystemsfrom,amongothers,theabilitytoadaptoperations

- 配套讲稿:

如PPT文件的首页显示word图标,表示该PPT已包含配套word讲稿。双击word图标可打开word文档。

- 特殊限制:

部分文档作品中含有的国旗、国徽等图片,仅作为作品整体效果示例展示,禁止商用。设计者仅对作品中独创性部分享有著作权。

- 关 键 词:

- 中级会计学 intermediate accounting 赖红宁 chapter 4课后答案 中级 会计学 课后 答案

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

《Java程序设计》考试大纲及样题试行.docx

《Java程序设计》考试大纲及样题试行.docx

-

《工业企业管理》自学任务书.docx

-

《短歌行》原文翻译及赏析.docx

-

《跳水》教案3.docx

-

《基于MATLAB的信号与系统实验指导》编程练习.docx

-

《你是最棒的》教学设计.docx

-

《选修4化学反应原理》知识点总结整理超全.docx

-

2环境应急监测试题资料.docx

-

《自动化仪表工程施工及验收规范》GB50093仪表安装检验批.docx

-

09年法律硕士民法预热辅导第2102讲完整篇doc.docx

-

6阅读能力阅读方法指什么.docx

-

《豆蔻镇的居民和强盗》读后感.docx

-

CMYK色值参考.docx

-

3121护理查对制度.docx

-

《草莓》课堂教学课件5篇.docx

-

CCNA完整知识点.docx

-

《合理安排时间》说课稿.docx

-

18我的伯父鲁迅先生.docx

-

3dmax授课计划doc.docx

-

《中共中央国务院关于加快推进生态文明建设的意见》.docx

-

《永生的眼睛》练习题附答案.docx

-

flow3d官方培训教程中的实例中文说明.docx

-

《宪法》《监察法》应知应会100题含答案.docx

-

EMS基础知识综合练习复习资料.docx

-

100以内退位减法500道带竖式空间可直接打印.docx

-

207声屏障施工组织设计.docx

-

30个科学小常识教学提纲.docx

-

JGJ59建筑施工安全检查标准评分表全套.docx

-

12幼儿园保育员培训活动记录表.docx

-

minecraft匠魂教程.docx

-

c语言课程设计学生成绩管理系统.docx

-

0503新闻传播学基本要求.docx

-

财务入职培训3篇范文模板 9页.docx

-

沈绍功教授月经病的治疗.docx

-

学生宿舍管理系统数据库课程设计.docx

-

外文资料翻译股利政策毕业论文.docx

-

数控毕业生实习报告.docx

-

X射线检验作业指导书.docx

-

《论语别裁》读后感5篇.docx

-

社团申请书1000字范文最新版大全.docx

-

企业所得税消费税 避税与反避税.docx

-

主要污染工序.docx

-

《送东阳马生序》及其历年考题.docx

-

透水性沥青混凝土面层.docx

-

汽车维修质量保证体系构建.docx

-

数字通信原理与技术王兴亮第 1 章绪论解析.docx

-

《企业运营与发展》形考试题及答案.docx

-

Historical geography.docx

-

XX年高考安徽卷语文复习系列教案.docx

-

中国民歌.docx

-

医用电气设备电磁兼容EMS试验中基本性能.docx

链接地址:https://www.bdocx.com/doc/8687021.html

党支部书记抓基层党建工作述职报告.docx

党支部书记抓基层党建工作述职报告.docx

- 最新西师版数学四年级下册教案Word文档下载推荐.docx

- 尊敬的各位老师大家下午好今天我就小学英语中的语音Word文件下载.docx

- 最新经济法基础模拟试题与答案文档格式.docx

- 最新高一数学上学期期中检测必修1+数学试题3优秀名师资料Word格式文档下载.docx

- 装配式结构住宅楼脚手架搭设方案Word格式文档下载.docx

- 最新人教部编版小学语文四年级上册21古诗三首说课稿Word格式文档下载.docx

- 重庆市中考英语真题试题A卷含答案新文档格式.docx

- 专题71 力考点题型解密解析版Word文档格式.docx

- 总务护士工作总结范文五篇Word格式.docx