Finc301Spring11FinalExam 1.docx

Finc301Spring11FinalExam 1.docx

- 文档编号:23608357

- 上传时间:2023-05-19

- 格式:DOCX

- 页数:15

- 大小:140.76KB

Finc301Spring11FinalExam 1.docx

《Finc301Spring11FinalExam 1.docx》由会员分享,可在线阅读,更多相关《Finc301Spring11FinalExam 1.docx(15页珍藏版)》请在冰豆网上搜索。

Finc301Spring11FinalExam1

NewYorkInstituteofTechnology

NanjingCampus

FINC301–InternationalFinanceManagement

Spring2011

FinalExam

Name:

________________________

Class:

________________________

NYITID#:

____________________

SectionA:

(35Questions–70points)

CIRCLEtheletteroftheonecorrectanswerONLY.DoNOTwriteanylettersanywhereinthissection!

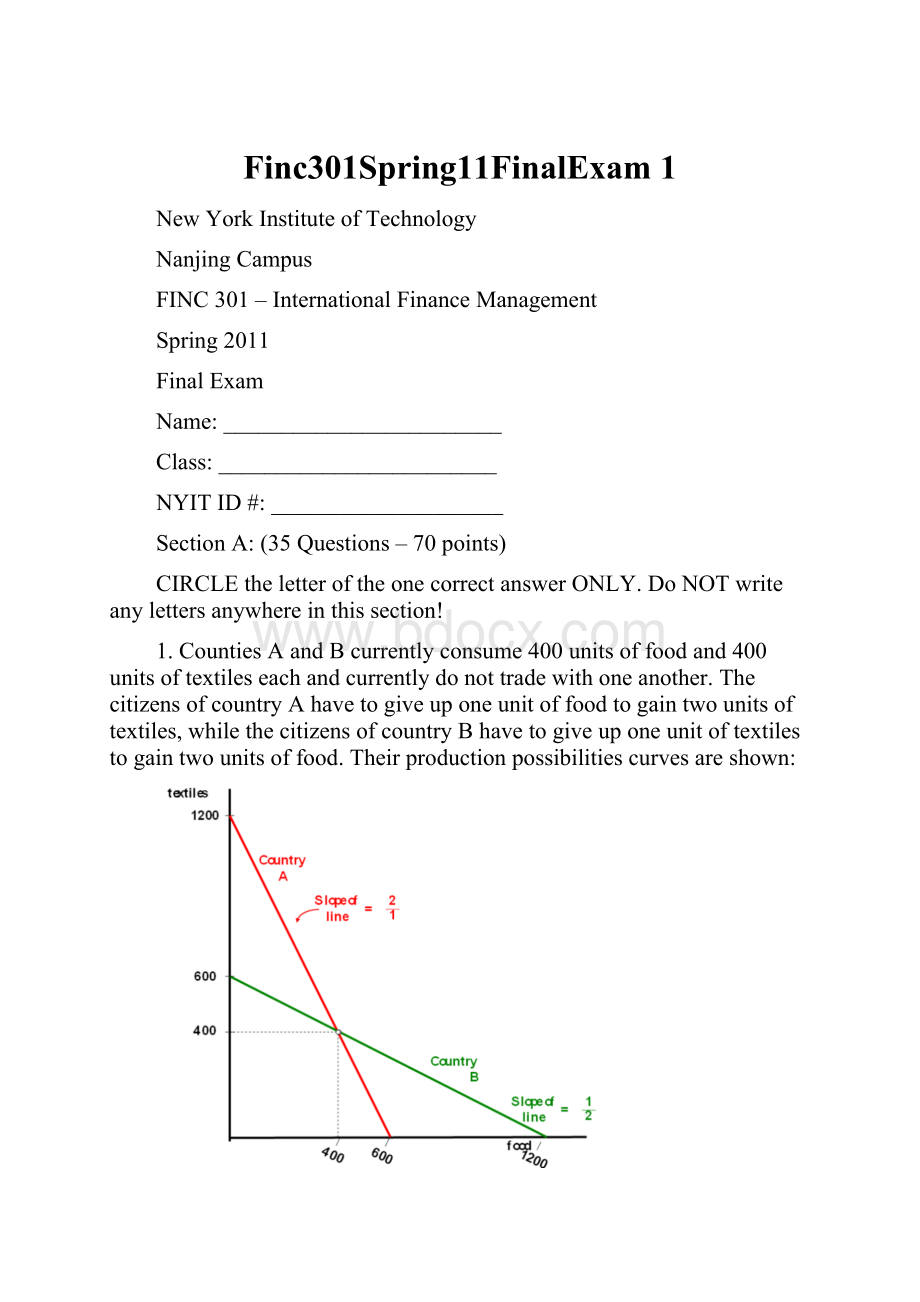

1.CountiesAandBcurrentlyconsume400unitsoffoodand400unitsoftextileseachandcurrentlydonottradewithoneanother.ThecitizensofcountryAhavetogiveuponeunitoffoodtogaintwounitsoftextiles,whilethecitizensofcountryBhavetogiveuponeunitoftextilestogaintwounitsoffood.Theirproductionpossibilitiescurvesareshown:

Underthetheoryofcomparativeadvantage,iffreetradeisallowed,themarketclearingprice(orexchangerateifyouwill)betweenfoodandtextileswillbe

A. Oneunitoffoodforoneunitoftextiles

B. SomewherebetweenOneunitoffoodfortwounitsoftextilesandtwounitsoffoodforoneunitoftextiles

C. Oneunitoffoodfortwounitsoftextiles

D. Twounitsoffoodforoneunitoftextiles

2.Consideradentistanda14-yearoldboy.Thedentistcanmake$100perhourdrillingteethandthe14-yearoldboycanmake$2perhourpickingupusedaluminumcans.Thedentistisamanlymanandcanmowhishalf-acrelotinonehour.The14-yearoldboycanmowthelawnintwohours.Ifthedentisthirestheboytomowhislawnatanypricelessthan$100,butmorethan$4:

A. Bothheandtheboyarebetteroff.

B. Thedentistwouldbeexploitingtheboy.

C. Theboywouldbeexploitingthedentist.

D. Alloftheabove.

3.Theinternationalmonetarysystemwentthroughseveraldistinctstagesofevolution.Thesestagesaresummarized,inalphabeticorder,asfollows:

(i)Bimetallism

(ii)BrettonWoodssystem

(iii)Classicalgoldstandard

(iv)Flexibleexchangerateregime

(v)Interwarperiod

Thechronologicalorderthattheyactuallyoccurredis:

A. (iii),(i),(iv),(ii),and(v)

B. (i),(iii),(v),(ii),and(iv)

C. (vi),(i),(iii),(ii),and(v)

D. (v),(ii),(i),(iii),and(iv)

4.Supposethatthepoundispeggedtogoldat£20perounceandthedollarispeggedtogoldat$35perounce.Thisimpliesanexchangerateof$1.75perpound.Ifthecurrentmarketexchangerateis$1.80perpound,howwouldyoutakeadvantageofthissituation?

Hint:

assumethatyouhave$350availableforinvestment.

A. Startwith$350.Buy10ouncesofgoldwithdollarsat$35perounce.Convertthegoldto£200at£20perounce.Exchangethe£200fordollarsatthecurrentrateof$1.80perpoundtoget$360.

B. Startwith$350.Exchangethedollarsforpoundsatthecurrentrateof$1.80perpound.Buygoldwithpoundsat£20perounce.Convertthegoldtodollarsat$35perounce.

C. a)andb)bothwork

D. Noneoftheabove.

5.Acountryexperiencingasignificantbalance-of-paymentssurpluswouldbelikelyto

A. Expandimports,offeringmarketingopportunitiesforforeignenterprises.

B. Unlikelytoimposeforeignexchangerestrictions.

C. Expandexports,offeringinternationalmarketingopportunitiesfordomesticenterprises.

D. Botha)andb)

6.Whenacountry’scurrencydepreciatesagainstthecurrenciesofmajortradingpartners,

A. Thecountry’sexportstendtoriseandimportsfall.

B. Thecountry’sexportstendtofallandimportsrise.

C. Thecountry’sexportstendtoriseandimportsrise.

D. Thecountry’sexportstendtofallandimportsfall.

7.ThedifferencebetweenForeignDirectInvestmentandPortfolioInvestmentisthat:

A. PortfolioInvestmentmostlyrepresentsthesaleandpurchaseofforeignfinancialassetssuchasstocksandbondsthatdonotinvolveatransferofcontrol.

B. ForeignDirectInvestmentmostlyrepresentsthesaleandpurchaseofforeignfinancialassetssuchasstockswhereasPortfolioInvestmentmostlyinvolvesthesalesandpurchaseofforeignbonds.

C. Foreigndirectinvestmentisaboutbuyinglandandbuildingfactories,whereasportfolioinvestmentisaboutbuyingstocksandbonds.

D. Alloftheabove

8.Inthecontextofinvestmentsinsecurities(stocksandbonds),portfolioriskdiversificationrefersto:

A. thetime-honoredadage"Don'tputallyoureggsinonebasket"

B. investors'abilitytoreduceportfolioriskbyholdingsecuritiesthatarelessthanperfectlypositivelycorrelated

C. thefactthatthelesscorrelatedthesecuritiesinaportfolio,thelowertheportfoliorisk

D. Alloftheabove

9.Studiesshowthatinternationalstockmarketstendtomovemorecloselytogetherwhenthevolatilityishigher.Thisfindingsuggeststhat

A. Investorsshouldliquidatetheirportfolioholdingsduringturbulentperiods.

B. Sinceinvestorsneedriskdiversificationmostpreciselywhenmarketsareturbulent,theremaybelessbenefittointernationaldiversificationforinvestorswholiquidatetheirportfolioholdingsduringturbulentperiods.

C. Thiskindofcorrelationiswhyinternationalportfoliodiversificationissmartfortoday'sinvestor.

D. Noneoftheabove

10.Theadjustedpresentvalue(APV)modelthatissuitableforanMNCisthebasicnetpresentvalue(NPV)modelexpandedto:

A.distinguishbetweenthemarketvalueofaleveredfirmandthemarketvalueofanunleveredfirm

B.discerntheblockingofcertaincashflowsbythehostcountryfrombeinglegallyremittedtotheparent

C.considerforeigncurrencyfluctuationsorextrataxesimposedbythehostcountryonforeignexchangeremittances

D.Alloftheabove

11.Iftheinvestorhedgestheexchangerateriskwheninvestinginternationally:

A. Therisk-returnefficiencyislikelytobesuperior.

B. TheexpectedreturntotheU.S.dollarinvestorisapproximatelythesamewhethertheinvestorhedgestheexchangerateriskintheinvestment,orremainsunhedged.

C. Totheextentthattheinvestorestablishesaneffectivehedgetoeliminateexchangerateuncertainty,theriskwillbereduced.

D. Alloftheabove

12.ConsiderasimpleexchangeriskhedgingstrategyinwhichtheU.S.dollarbasedinvestorsellstheexpectedforeigncurrencyproceedsofariskyinvestmentforward.AlthoughtheexpectedforeigninvestmentproceedswillbeconvertedintoU.S.dollarsattheknownforwardexchangerateunderthisstrategy,theunexpectedforeigninvestmentproceeds

A. WillhavetobeconvertedintoU.S.dollarsattheuncertainforwardspotexchangerate.

B. WillhavetobeconvertedintoU.S.dollarsattheuncertainfuturespotexchangerate.

C. WillhavetobeconvertedintoU.S.dollarsattheuncertainswapexchangerate.

D. Noneoftheabove.

13.Abankmayestablishamultinationaloperationforthereasonofriskreduction.Theunderlyingrationalebeing:

A. Bymaintainingforeignbranchesandforeigncurrencybalances,banksmayreducetransactioncostsandforeignexchangeriskoncurrencyconversionifgovernmentcontrolscanbecircumvented.

B. Greaterstabilityofearningsispossiblewithinternationaldiversification.Offsettingbusinessandmonetarypolicycyclesacrossnationsreducesthecountry-specificriskofanyonenation.

C. Multinationalbanksareoftennotsubjecttothesameregulationsasdomesticbanks.Theremaybereducedneedtopublishadequatefinancialinformation,lackofrequireddepositinsuranceandreserverequirementsonforeigncurrencydeposits,andtheabsenceofterritorialrestrictions.

D. Multinationalbankingoperationshelpabankpreventtheerosionofitstraveler'scheck,tourist,andforeignbusinessmarketsfromforeignbankcompetition.

14.Thecurrentexchangerateis€1.00=$1.50.ComputethecorrectbalancesinBankA'scorrespondentaccount(s)withbankBifacurrencytraderemployedatBankAbuys€100,000fromacurrencytraderatbankBfor$150,000usingitscorrespondentrelationshipwithBankB.

A. BankA'sdollar-denominatedaccountatBwillfallby$150,000.

B. BankB'sdollar-denominatedaccountatAwillfallby$150,000.

C. BankA'spound-denominatedaccountatBwillfallby€100,000.

D. BankB'spound-denominatedaccountatAwillriseby€100,000.

15.A"threeagainstnine"forwardrateagreement,

A. Couldcallforabuyertosellasix-monthEurobondinthreemonthsatpricesagreedupontoday.

B. Isaforwardcontractonathree-monthEurobondwithanine-monthmaturity.

C. Couldcallforabuyertopaythesellertheincreasedinterestcostonanotationalamountifsix-monthinterestratesfallbelowanagreedratebeginningthreemonthsfromnowandendingninemonthsfromnow.

D. Isaforwardcontractonanine-monthEurobondwithathree-monthmaturity

16.Onelessonfromthecreditcrunchisthat

A. Intheaggregate,creditscorestendtounderstatetheprobabilityofdefault—therebyapoolofsubprimemortgagesisactuallyquiteasafeinvestmentsincenoteveryborrowerdefaults.

B. Moralhazard,whileanissueinthemarketforusedcars,doesnotseemtoaffecttheU.S.financialsystemduetotheeffectiveregulatoryenvironment.

C. BankersseemnottoscrutinizecreditriskascloselywhentheyserveonlyasmortgageoriginatorsandthenpassitontoMBSinvestorsratherthanholdthepaperthemselves.

D. Noneoftheabove

17.Withregardtoclearingproceduresforbondtransactions,whenatransactionisconducted,electronicbookentriesaremadethattransferbookownershipofthebondcertificatesfromthesellertothebuyerandtransferfundsfromthepurchaser'scashaccounttotheseller's.However,

A.Physicaltransferofthebondsseldomtakesplace.

B. Thephysicaltransferofthebondstakesplaceasmuchas3dayslater.

C. Thephysicaltransferofthebondstakesplaceasmuchas6weekslater.

D. T

- 配套讲稿:

如PPT文件的首页显示word图标,表示该PPT已包含配套word讲稿。双击word图标可打开word文档。

- 特殊限制:

部分文档作品中含有的国旗、国徽等图片,仅作为作品整体效果示例展示,禁止商用。设计者仅对作品中独创性部分享有著作权。

- 关 键 词:

- Finc301Spring11FinalExam

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

《酒店人力资源管理》教案.docx

《酒店人力资源管理》教案.docx

-

《马克思主义基本原理概论》选择题复习题.docx

-

《全国100所名校示范卷》高三生物人教版西部卷一轮复习 第十五单元 《稳态与环境》综合检测.docx

-

《1吨有多重》教学设计反思及评点2篇.docx

-

《红飘带狮王》读书笔记.docx

-

《教综》真题答案.docx

-

《企业管理》复习题发学生.docx

-

《提高数学学困生的学习兴趣研究》课题工作总结报告.docx

-

《蟋蟀的住宅》的教学设计.docx

-

《园林建筑设计》教案.docx

-

《中西医结合内科学》精华笔记.docx

-

2三轴向加速度传感器长春汽车工业高等专科学校.docx

-

04装修工程施工合同.docx

-

5套打包四年级数学上期中考试单元综合练习题含答案解析.docx

-

《食品安全法》知识竞赛题目及答案.docx

-

《24式简化太极拳》简案.docx

-

《金融理论与实务》复习大纲.docx

-

《旅游地理》学案.docx

-

《企业集团财务管理》综合练习题参考答案11春.docx

-

《实践论》原文毛泽东.docx

-

《项目管理软件》课程复习题.docx

-

《员工手册》电子版范文.docx

-

《中小学布局整改措施》.docx

-

5旋风分离器安装.docx

-

10kV跨越架搭设施工方案设计.docx

-

#市关爱儿童服务中心暨救助站改造工程项目建议书.docx

-

《毛概》课程标准.docx

-

《人民日报》学习贯彻党的十七届四中全会精神系列.docx

-

《我的军训生活》作文800字.docx

-

《研发人员绩效考核奖励办法》.docx

-

1 《道路交通安全法》规定任何单位或者个人不得收缴机.docx

-

02电气检修规程.docx

-

余热回收设计方案.docx

-

小说的考察题型及方法.docx

-

中国医疗卫生服务业的现状.docx

-

新版pep小学三年级英语下册第六单元教案三维目标.docx

-

新人教版学年八年级下学期期末物理试题II卷.docx

-

学生个人实习计划1.docx

-

烟台市初中化学学业考试带答案.docx

-

一年级美术综合实践活动教学计划doc资料.docx

-

医疗质量万里行活动方案.docx

-

中考备考会议新闻稿大全.docx

-

义务兵入团申请书范文三篇.docx

-

造价员个人述职报告.docx

-

最新太空泥教案资料.docx

-

整理生物必修二期末测试题二汇总.docx

-

职业健康安全重大危险源清单.docx

-

35kV高压线路三段式电流保护系统设计.docx

-

中医病情观察望闻问切试题1.docx

-

《基础护理学》教学大纲.docx

-

《医疗机构从业人员行为规范》.docx