introduction to managerial accounting ch2.docx

introduction to managerial accounting ch2.docx

- 文档编号:26716544

- 上传时间:2023-06-22

- 格式:DOCX

- 页数:12

- 大小:307.06KB

introduction to managerial accounting ch2.docx

《introduction to managerial accounting ch2.docx》由会员分享,可在线阅读,更多相关《introduction to managerial accounting ch2.docx(12页珍藏版)》请在冰豆网上搜索。

introductiontomanagerialaccountingch2

ManagerialCostConceptsandCostBehaviourAnalysis

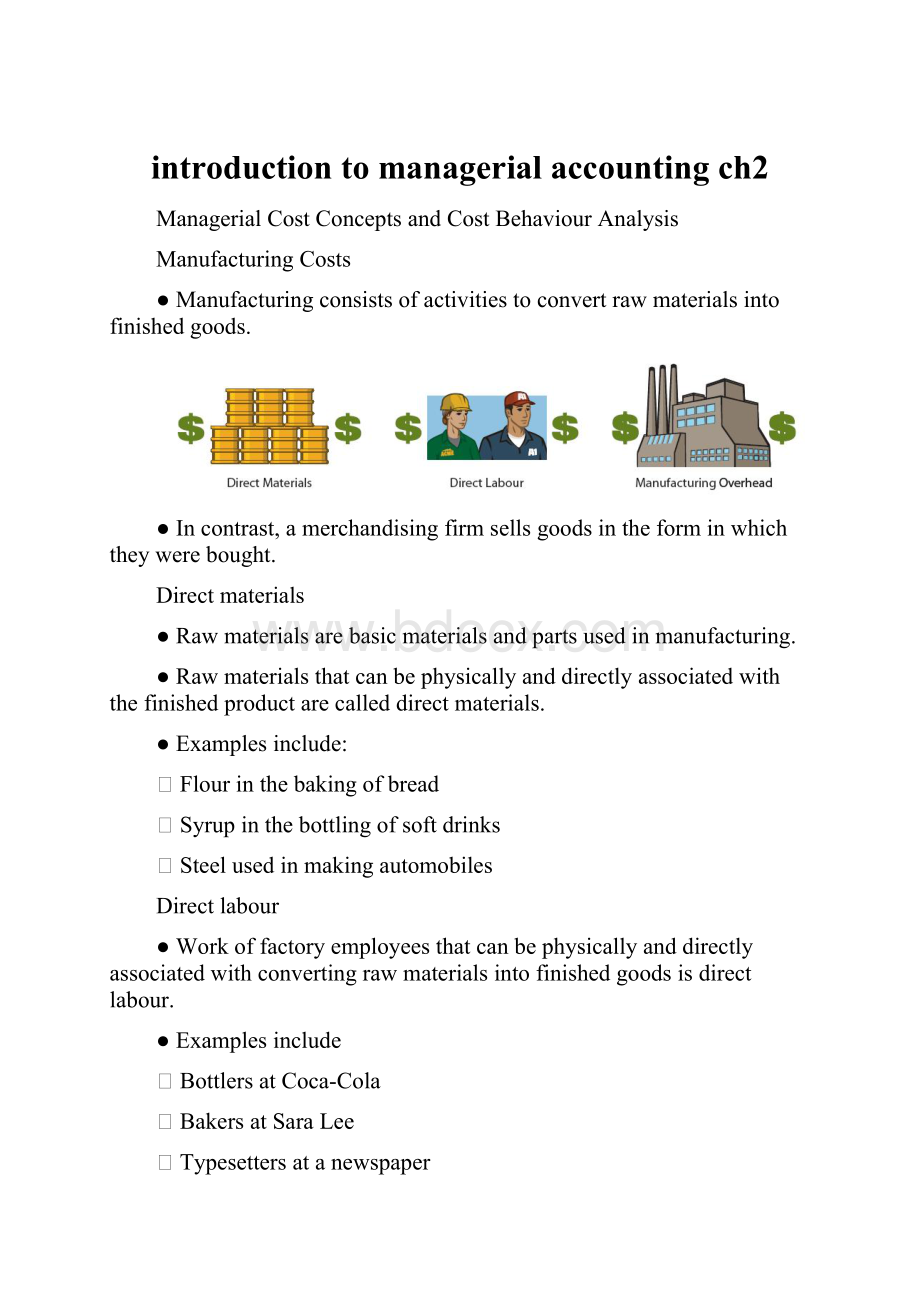

ManufacturingCosts

●Manufacturingconsistsofactivitiestoconvertrawmaterialsintofinishedgoods.

●Incontrast,amerchandisingfirmsellsgoodsintheforminwhichtheywerebought.

Directmaterials

●Rawmaterialsarebasicmaterialsandpartsusedinmanufacturing.

●Rawmaterialsthatcanbephysicallyanddirectlyassociatedwiththefinishedproductarecalleddirectmaterials.

●Examplesinclude:

⏹Flourinthebakingofbread

⏹Syrupinthebottlingofsoftdrinks

⏹Steelusedinmakingautomobiles

Directlabour

●Workoffactoryemployeesthatcanbephysicallyanddirectlyassociatedwithconvertingrawmaterialsintofinishedgoodsisdirectlabour.

●Examplesinclude

⏹BottlersatCoca-Cola

⏹BakersatSaraLee

⏹Typesettersatanewspaper

ManufacturingOverhead

●Coststhatareindirectlyassociatedwithmanufacturingoffinishedgoods

●Allmanufacturingcoststhatcannotbeclassifiedasdirectmaterialanddirectlabour

●Examplesinclude:

⏹Indirectmaterials

⏹Indirectlabour

⏹Amortizationonfactorybuildings,insurance,taxes,maintenanceonfactoryfacilities.

Indirectmaterials

●Rawmaterialsthatcannotbeeasilyassociatedwiththefinishedproductarecalledindirectmaterials

●Indirectmaterialsdonotphysicallybecomepartofthefinishedproductorrepresenttoosmallapartofthefinishedproductintermsofcost

●Consideredpartofmanufacturingoverhead

●Examplesinclude:

⏹Lubricants

⏹Cleaningsupplies

⏹Polishingcompounds

Indirectlabour

●Workoffactoryworkersthathavenophysicalassociationwiththefinishedproduct,orforwhichitisimpracticaltotracetothegoodsproduced,isindirectlabour

●Examplesinclude:

⏹Wagesofmaintenanceworkers,janitors,andsecurityguards

⏹Supervisors

⏹Time-Keepers

PrimeCostsandConversionCosts

●Primecostsarethesumofalldirectmaterialscostsanddirectlabourcosts.Thesearealldirectmanufacturingcosts.

●Conversioncostsarethesumofalldirectlabourcostsandmanufacturingoverheadcosts,whichtogetherarethecostsofconvertingrawmaterialsintoafinalproduct.

ProductCosts

●Consistsofthedirectmaterialcost,thedirectlabourcost,andthemanufacturingoverheadcost

●Anecessaryandintegralpartofproducingtheproduct

●Recordedasinventorywhenincurred

●Donotbecomeexpenseuntilthefinishedgoodinventoryissold

PeriodCost

●Matchedwithrevenueofaspecifictimeperiodandchargedtoexoenseasincurred

●Non-manufacturingcosts

●Deductedfromrevenuesinperiodincurredtodeterminenetincome

●Includeall

⏹Sellingexpenses

⏹GeneralandAdministrativeexpenses

ProductversusPeriodCosts

CostBehaviourAnalysis

●Definition:

Thestudyofhowspecificcostsrespondtochangesinthelevelofbusinessactivity

●Somecostschange;othersremainthesame

●Helpsmanagementplanoperationsandmakedecisions

●Appliestoalltypesofbusinessesandentities

●Startingpointismeasuringkeybusinessactivities

●Activitylevelsmaybeexpressedintermsof

⏹Salesdollars(inaretailcompany)

⏹Kilometersdriven(inatruckingcompany)

⏹Roomoccupancy(inahotel)

⏹Danceclassestaught(byadancestudio)

●Foranactivityleveltobeuseful,changesinthelevelorvolumeofactivityshouldbecorrelatedwithchangesincost

●Theactivitylevelselectediscalledtheactivity(orvolume)index

⏹Identifiestheactivitythatcauseschangesinthebehaviourofcosts

⏹Allowscoststobeclassifiedaccordingtotheirresponsetochangesinactivityas:

VariableCost

FixedCost

MixedCost

VariableCost

●Coststhatvaryintotaldirectlyandproportionatelywithchangesintheactivitylevel

●Iftheactivitylevelincreases10%,totalvariablecostsincrease10%;iftheactivityleveldecreaseby25%,totalvariablecostswilldecreaseby25%

●Variablecostsalsoremainconstantperunitateverylevelofactivity

●Examplesofvariablecostsinclude:

⏹Directmaterialanddirectlabourforamanufacturer

⏹Salescommissionsforamerchandiser

⏹Gasolineinairlinesandtruckingcompanies

Examples:

◆DamonCompanymanufacturesratiosthatcontaina$10clock

◆Activityindexisthenumberofradiosproduced

◆Foreachradioproduced,thetotalcostoftheclocksincreasesby$10

✧If2,000radiosaremade,thetotalcostoftheclocksis20,000(2,000x$10)

✧If10,000radiosaremade,thetotalcostoftheclocksis$100,000

(10,000x$10)

FixedCosts

●Coststhatremainthesameintotalregardlessofchangesintheactivitylevel.

●Perunitcostvariesinverselywithactivity:

⏹Asvolumeincreases,unitcostdecline,andviceversa

●Examplesinclude:

⏹Propertytaxes

⏹Insurance

⏹Rent

⏹Amortizationonbuildingsandequipment

Examples:

◆DamonCompanyleasesitsproductivefacilitiesfor$10,000permonth

◆Totalfixedcostsofthefacilitiesremainconstantatalllevelsofactivity-$10,000permonth

◆Onaperunitbasis,thecostofrentdecreasesasactivityincreasesandviceversa

✧At2,000radios,theunitcostis$5($10,000÷2,000units)

✧At10,000radios,theunitcostis$1($10,000÷10,000units)

DistinguishBetweenVariableandFixedCosts

●Variablecostsarecoststhatvaryintotaldirectlyandproportionatelywithchangesintheactivitylevel.Thesecostsremainthesameperunitateverylevelofactivity.

●Fixedcostsarecoststhatremainthesameintotalwithintherelevantrangeregardlessofthechangesintheactivitylevel.Fixedcostsperunitvaryinverselywithactivity–inotherwordsasvolumeincreases,unitcostsdecreaseandviceversa.

RelevantRange

●Throughouttherangeofpossiblelevelsofactivity,astraight-linerelationshipusuallydoesnotexistforeithervariablecostsorfixedcosts

⏹Therelationshipbetweenvariablecostsandchangesinactivitylevelisoftencurvilinear

⏹Forfixedcosts,therelationshipisnonlinear–somefixedcostswillnotchangeovertheentirerangeofactivities,othersmaychangeatdifferentlevelsofactivity

●Definedastherangeofactivityoverwhichacompanyexpectstooperateduringayear

●Withinthisrange,astraight-linerelationshipusuallyexistsforbothvariableandfixedcosts

MixedCosts

●Coststhathavebothavariablecostelementandafixedcostelement

●Sometimescalledsemivariablecost

●Changeintotalbutnotproportionatelywithchangesinactivitylevel

High-LowMethod

●Mixedcostsmustbeclassifiedintotheirfixedandvariableelements

●Oneapproachtoseparatethecostiscalledthehigh-lowmethod

⏹Usesthetotalcostsincurredatboththehighandthelowlevelsofactivitytoclassifymixedcosts

⏹Thedifferenceincostsbetweenthehighandlowlevelsrepresentsvariablecosts,sinceonlyvariablecostschangeasactivitylevelschange

⏹Steps:

1.Determinevariablecostperunitusingthefollowingformula:

2.Determinethefixedcostbysubtractingthetotalvariablecostateitherthehighorthelowactivitylevelfromthetotalcostatthelevel

Example:

◆DataforMetroTransitCompanyforthelast4-monthperiod:

HighLevelofActivity:

April$63,000100,000km

LowLevelofActivity:

January30,00040,000km

Difference:

$33,00060,000km

1.Usingtheformula,variablecostsperunitare$33,000÷60,000=$.55variablecostperkm

ActivityLevel

High

Low

TotalCost

$63,000

$30,000

Less:

Variablecosts

(100,000x$.55)

55,000

(40,000x$.55)

22,000

Totalfixedcosts

$8,000

$8,000

2.Subtracttotalvariablecostsateitherthehighorlowactivitylevelfromthetotalcostatthatsamelevel

Example:

iftheactivitylevelis45,000km,theestimatedmaintenancecostswouldbe$8,000fixedand$24,750variable($.55x45,000km)foratotalof$32,750

ManufacturingCostsinFinancialStatement

Incomestatement

●Theincomestatementforamanufacturerissimilartothatofamerchandiserexceptforthecostofgoodssoldsection

CostsofGoodsSoldSectionoftheIncomeStatement

DeterminetheCostofGoodsManufactured

●WorkinProcess–partiallycompletedunitsofaproduct

●TotalManufacturingCosts–sumofdirectmaterialcosts,directlabourcosts,andmanufacturingoverhead,allincurredduringthecurrentyear

CostofGoodsManufacturedSchedule

BalanceSheet

Inventories

●Manufacturingcompaniesmayhavethreeinventoryaccounts:

⏹Rawmaterialsinventory–showsthecostofrawmaterialsonhand

⏹Workinprocessinventory–showsthecostapplicabletounitsonwhichproductionhasstartedbutisonlypartiallycomplete

⏹Finishedgoodsinventory–showsthecostofcompletedgoodsonhand

●Merchandisingcompanieshaveonlyonecategoryofinventory

⏹Merchandiseinventory

- 配套讲稿:

如PPT文件的首页显示word图标,表示该PPT已包含配套word讲稿。双击word图标可打开word文档。

- 特殊限制:

部分文档作品中含有的国旗、国徽等图片,仅作为作品整体效果示例展示,禁止商用。设计者仅对作品中独创性部分享有著作权。

- 关 键 词:

- introduction to managerial accounting ch2

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

冰豆网所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

《C12343098汽轮机操作规程》要点.docx

《C12343098汽轮机操作规程》要点.docx

-

《钢丝绳芯输送带硫化接头标准》.docx

-

《建筑装饰CAD》课程标准.docx

-

《劳动合同书》范本下载.docx

-

《普通话实用训练教程》教案 1.docx

-

《上海星河湾土方道路景观铺装景观建筑景观小品绿化种植及配套水电安装工程施工组织设计》教学.docx

-

#2#014年护士执业资格考试考前押题卷实践能力.docx

-

《繁荣世界守护者》图文流程攻略.docx

-

《工业设计机械基础》复习题.docx

-

《机电一体化系统设计》思考题.docx

-

《Java项目实训》课程设计计算器要点.docx

-

《赤壁赋》必修一9.docx

-

《工商企业经营管理》重点复习题供参考.docx

-

《审计准则第1322号公允价值计量和披露的审计》指南全解.docx

-

《索溪峪的野》课堂教学实录文档资料.docx

-

《餐饮服务与管理》教学计划复习进程.docx

-

《花卉栽培》试题库完整.docx

-

《经络学B》答案.docx

-

《身边地化学物质》知识点汇总情况.docx

-

《5鲁滨逊漂流记》教学设计和教案附同步练习.docx

-

《送别组诗》教案.docx

-

《Visual Basic程序设计基础》课后习题参考答案.docx

-

《创新与企业家精神》.docx

-

《詹天佑》教学反思说课稿教学设计教材.docx

-

《风力发电机组设计方案与制造》课程设计方案任务书.docx

-

《最后的姿势》教学设计.docx

-

1楼无机保温砂浆外墙外保温涂料饰面1分解.docx

-

5篇学校工作开展情况述职报告.docx

-

6届高三上学期一轮纠错生物试题附答案.docx

-

《图书馆学概论》知识点.docx

-

《语言学导论》期末复习及练习.docx

-

02煤矿电能质量治理技术的研究与应用计划任务书.docx

-

班会发言致辞大全.docx

-

市长在全市金融工作会议上的重要说话发言.docx

-

真题及答案.docx

-

适合做各种场合的背景音乐世界上最好的音乐大集合精品资料.docx

-

整理党风廉政建设责任制汇报提纲.docx

-

竖井施工交底.docx

-

水产品销售合同模板.docx

-

正能量故事.docx

-

司法实践各类案件证据提交清单.docx

-

北大教授批贾康著作.docx

-

四川省雅安市天全中学学年高二英语上学期期中试题.docx

-

四年级下册《语文园地四》教案.docx

-

职称英语考试理工类A级考前精准押题试题及答案最后一套.docx

-

苏教版二年级 语文第一单元备课.docx

-

苏宿园区园区公舍无线智能消防报警系统采购安装项目招标文件模板.docx

-

职业演讲稿范文4篇.docx

-

探讨建筑中绿色节的能技术的应用.docx

-

提高沟通协调能力做好办公室工作解析.docx

-

北京注协 工作总结.docx